In Democracy and the Market, Adam Przeworski argues that transitional countries experience a significant downturn in economic performance in the short term and then as democracy takes root, economic performance returns in ways that support the new democracy.

Watching events here in the UK since the EU referendum on 23 June, I couldn’t help feeling that the UK now looks very much like one of Przeworski’s transitional countries and is experiencing precisely the same kind of economic downturn as a result of the vote to leave the EU.

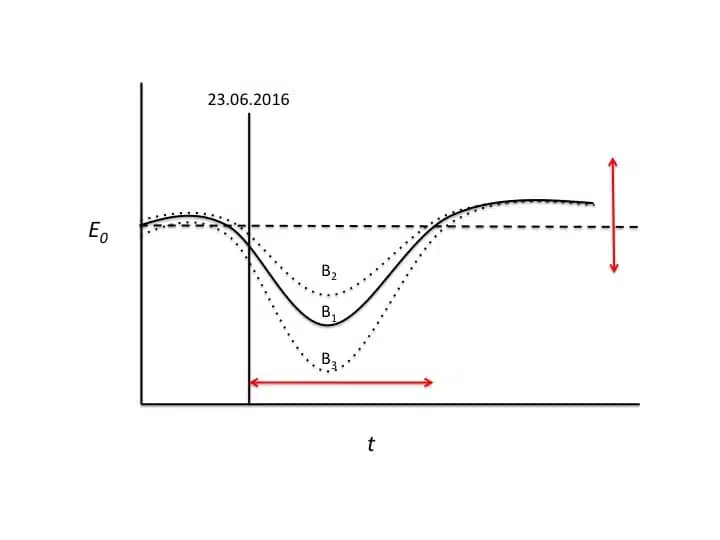

The figure below represents this dynamic. The y-axis represents economic performance (E), which would have remained relatively constant over time (t) had there not been an EU referendum. On 23 June, however, there was a referendum, which saw an economic pick up in the run up to the vote (a signal from the markets that Remain was the likely outcome), and a subsequent slowdown once the result of Leave became official on the morning of the 24th.

We now find ourselves in a significant ‘Brexit dip’ in economic performance (B). The pound against the dollar has dropped to levels not seen in thirty years (click HERE to track its value relative to other currencies), the FTSE 100 and, more importantly, the FTSE 250 have dropped precipitously, S & P dropped the UK from its AAA rating to an AA rating, while leaders of business surveyed by the Institute of Directors (IoD) are fairly pessimistic about the immediate future of the British economy. So much so, that many report a stall in investment, a freeze on hiring, and in some cases, redundancies.

We now find ourselves in a significant ‘Brexit dip’ in economic performance (B). The pound against the dollar has dropped to levels not seen in thirty years (click HERE to track its value relative to other currencies), the FTSE 100 and, more importantly, the FTSE 250 have dropped precipitously, S & P dropped the UK from its AAA rating to an AA rating, while leaders of business surveyed by the Institute of Directors (IoD) are fairly pessimistic about the immediate future of the British economy. So much so, that many report a stall in investment, a freeze on hiring, and in some cases, redundancies.

In addition to the economic downturn, we have seen both main political parties in crisis, as the struggle for power ensues. The Prime Minister has resigned, the shadow cabinet and junior shadow ministers have resigned, and there are fresh calls for Jeremy Corbyn to step down as leader of the Labour Party. The Leave campaign leaders are scrambling around to clarify what they actually mean by Brexit, the Remain campaign leaders are looking at legal loopholes and procedures that might reverse the decision, or at least limit its most negative consequences, and the Scots are exploring their own independence given their overwhelming vote to Remain.

The figure also shows a number of dimensions and possible scenarios for what could happen next. The dark line labelled B1 denotes a Brexit dip and long term recovery, which may see the UK return to economic performance levels that are higher than those before the referendum. Line B2 is a less severe Brexit dip that could be achieved through continued assurances from Bank of England Governor Mark Carney and the Chancellor of the Exchequer George Osbourne. B3 is a more severe Brexit dip if such overtures fail to calm market nerves and the UK economy slips further into recession. A Breixt dip is inevitable as many experts before the referendum pointed out, and any recovery carries risk and uncertainty with an eventual landing point that could vary substantially.

Both the depth and breadth of the Brexit dip rest on the ability of the UK political system to produce new leadership, trigger an Article 50 withdrawal from the EU, and establish an orderly timeline for how and under what conditions the UK will continue to work with the EU without being in the EU. Boris Johnson, the favourite for being the next Prime Minister signalled today that he would want the UK to continue its close cooperation with the EU, but did not spell out exactly what that might look like.

If Brexit really is going to happen (something the Scots are contesting), then it is incumbent on the new leadership to act quickly and decisively to bring certainty and confidence back to the UK economy. In seeking to prevent further disintegration, EU leaders will negotiate hard with the UK in setting conditions for access to the common market (e.g. national payments to the EU and free movement of labour). In preventing a total backlash from the Leave supporters, the new leadership in the UK will seek to maximise benefit from cooperation with the EU without having to incur too many costs.

One possible outcome for the future is the irony of the UK having to pay as much as it pays now and to accept only a minor reduction in migration, while at the same time having to give up its place at the EU table. The Leave campaign made a meal out of the crumbling castle of the EU and lambasted the Remain campaign’s insistence that the UK would be stronger in Europe, and yet the outcome of any Article 50 negotiations may well see the UK maintaining payments, accepting migrants, and losing influence. Meanwhile, one of the main societal group who voted for Leave will be very unlikely to see any real benefit from their vote.

References:

Adam Przeworski (1991) Democracy and the Market, Cambridge: Cambridge University Press.

Contact

T 07584 615104

E info@todd-landman.com

Keep In Touch

Todd Landman. All Rights Reserved

A Mackman Group collaboration - market research by Mackman Research | website design by Mackman